Yesterday, the GOP members of the Senate proposed their own tax overhaul, which differs from the GOP House proposal released last Thursday. The real question you might be asking how does this affect me if I’m in or near retirement?

We’ve looked through the different proposals and called out the parts most relevant for retirees, giving a rating of 💚 for what we liked and ❌ for what we didn’t like. For even more information, please check out this guide.

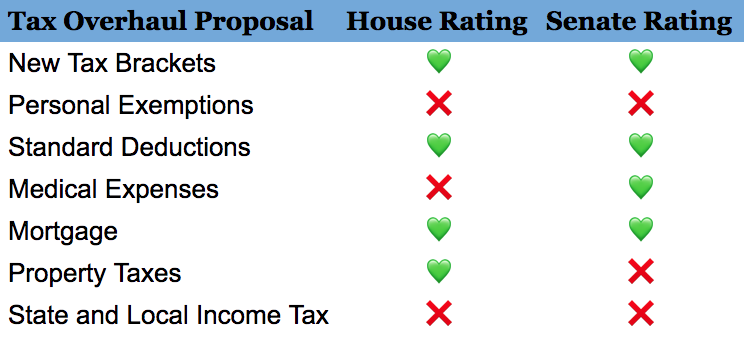

Tax Bracket

The first thing to consider is what tax bracket you’ll fall into with the proposed tax changes. Remember tax brackets are progressive, meaning if your annual income is $45,000, you don’t pay 25% federal taxes ($11,250). You pay 10% on the first $0-$9,525, 15% on the next $9,525-$38,700, and 25% on the final $38,700-$45,000 — totaling $6,903.

Single Filers

The House and Senate proposed tax brackets for single filers compared with with the current 2017 rates:

Married Filers

The new House and Senate tax bracket proposals for married filers:

Overall, the tax bracket proposals look beneficial to retirees, with the House proposal being better than the Senate proposal.

House and Senate Rating: 💚

What Else to Watch

Tax brackets aren’t the only thing to consider in the tax overhaul, especially for the retiree or those approaching retirement.

Personal Exemption

Both proposals remove the personal exemption. Currently, you can deduct $4,050 for oneself, spouse, and dependents. While the personal exemption is eliminated, the child and non-child dependent credits are increasing ($1,000 to $1,600 for the House and $1,650 for the Senate). However, if you are retired and no longer have dependents, this might not matter.

The House, but not the Senate, proposal does plan to give a $300 credit for oneself, spouse and dependents. Again, this won’t make up for the lost of personal exemption.

House and Senate Rating: ❌

Standard deduction

The standard deduction currently is $6,350 for single filers and $12,700 for married filers.

House and Senate Proposal: Increase to $12,000 for singles and $24,000 for married.

House and Senate Rating: 💚

Medical Expenses

Medical expenses can currently be deducted if you itemize, and this can be a large and important savings for retirees!

House proposal: Eliminate

Senate proposal: Keep

House rating: ❌, Senate rating: 💚

Mortgage and Property Tax

You can currently deduct both your mortgage and property taxes. If you are a homeowner, especially if you still have a mortgage, this is important.

House proposal: Keep mortgage (up to $500,000) and property tax (up to $10,000) deductions.

Senate proposal: Eliminate property tax deduction, but keep the mortgage deduction.

Mortgage House rating: 💚, Senate rating: 💚

Property Tax House rating: 💚, Senate rating: ❌

State and Local Income Tax

You can currently deduct both your state and local income taxes. This is a big benefit for those who living in high tax states such as New York, New Jersey, or California.

House and Senate proposal: Eliminate

House and Senate rating: ❌

So…

The question is are the proposals better or worse for those in or nearing retirement? Unfortunately, the answer is: it depends. It depends on your circumstances, such as do you live in a high tax state, have medical expenses, or take the standard deduction. For a lot of people, the tax changes will be beneficial. If you want to understand your current tax payment, try this calculator and be sure to keep an eye out for house these proposals make their way through the House and Senate.